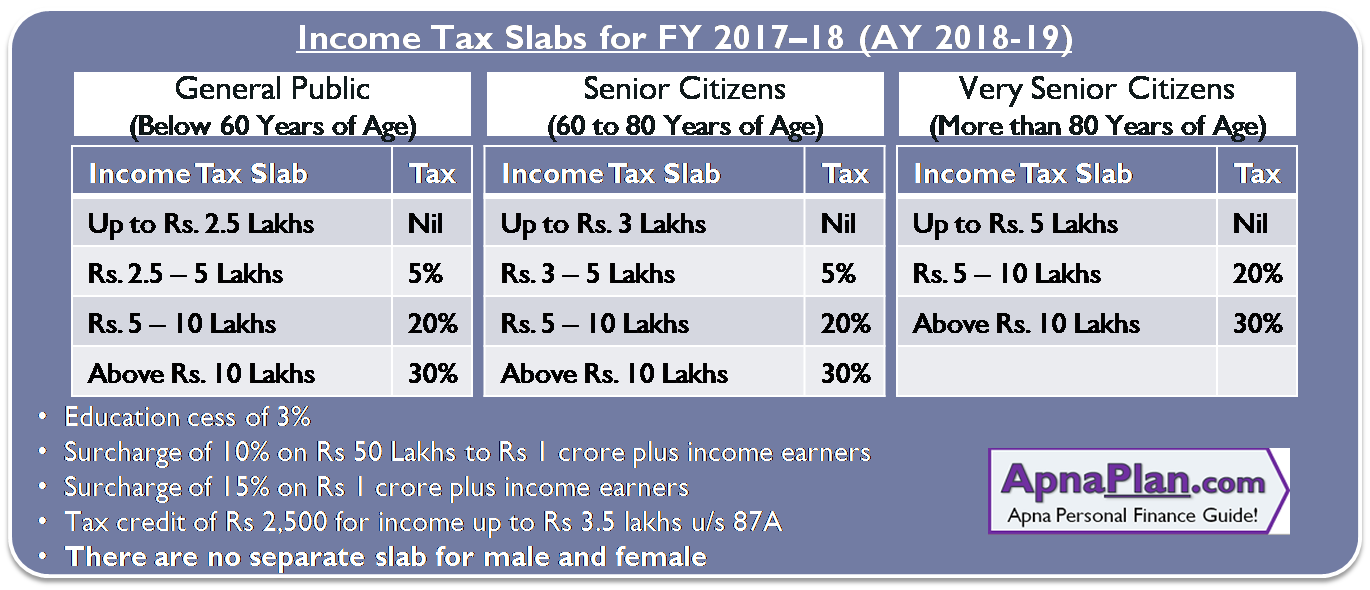

Table of Content

Though, the claim can only take place in the year in which the payment has been made. On the two self-occupied houses the maximum deduction for housing loan interest paid under section 24b is restricted to Rs.2 Lakhs per year for both houses taken together. Additionally, if the borrower sells his property within 5 years of taking the possession of the property, he cannot claim the 80C home loan deduction. Moreover, any deduction claimed by the borrower will be reversed in the year in which the property is sold and the same will reflect as income of the borrower in the year of sale of the property. Under this section, the maximum tax deduction is allowed Rs 1,50,000/- This is the section, where most of the people claim a deduction.

The deduction under 80EE is applicable only to individuals which means that if you are a HUF, AOP, a company, or any other kind of taxpayer, you cannot claim the benefit under this section. To claim this deduction, you should not own any other house property on the date of the sanction of a loan from a financial institution. If the spouse is a co-borrower, they can also file for tax deductions. In the case of a joint loan, both parties can claim their share of the loan they pay.

Home Loan Tax Benefits under Section 80C – Principal Deductions

This period starts from the end of the financial year in which the loan is borrowed. The deduction can be claimed from the year in which the construction is completed. If you have a second home that is unoccupied or houses dependents such as parents, you can claim a deduction on the interest paid on the second home loan under the same section. However, note that the total deduction on the interest paid on both Home Loans shouldn’t exceed INR 2 lakhs. Interest is allowed u/s 80EE only where loan has been taken from a financial institution or a housing finance company. Interest on loan from father is not eligible for exemption U/s 80EE.

Only those buyers can claim benefits under Section 80EEA who are not claiming deductions under Section 80EE.3. Property value should not exceed Rs 45 lakhs.4. Carpet area of the unit is limited to 60 sq metres in mega cities and 90 sq metres in other cities.5. The loan should have been taken from a bank or housing finance company and not from friends or family members. Suppose you buy a property that is being constructed and are currently paying the EMIs for the loan.

Ask a Chartered Accountant

You cannot claim house loan interest for the property which is not owned by you. Interest related to first home can be claimed according to your share. ITR-1/4 will be applicable if there is income from only one house property. While filing ITR of 17-18, I am showing my running home loan (as construction got completed in 17-18). Hence, I am filing 3 lakhs as home loan interest + 40,000/- (pre-construction).

Only interest amount paid on housing loan is allowed as deduction u/s 80EE. You can claim a deduction for each home loan separately, it will not be clubbed and allowed from only one single house property. Interest prior to the possession of house property has to be claimed in five equal instalments beginning from the F.Y. I am first-time house buyer and did not have any property on the date of sanction of loan.

Deductions under Section 80EE

The deduction is only possible after the house gets entirely completed and there is a completion certificate for the same. The principal amount paid on any under-construction structure/property is not going to be a part of this section. The Indian Income Tax Act has various provisions to reduce your tax liability by applying for rebates.

While a housing loan can help you get a house for yourself; it can also turn out to be an expensive affair. But the various tax benefits that come with such a loan help you save money every year. Take a look at how you can make the most of these benefits. Union Finance Minister Nirmala Sitharaman in the budget speech proposed to extend the deadline for availing additional deductions on interest payment on home loans to 31 March 2024.

Deductions allowed on home loan principal

This includes a maximum of Rs. 2 lakh on the interest paid and up to Rs. 1.5 lakh on the principal amount. Home Loan income tax rebate is also applicable on the interest paid. You can claim a maximum deduction of INR 2 lakhs under section 24 in a given financial year on a self-occupied property. Yes you are eligible to claim deduction under section 80EE if the value of your house property does not exceed rs. 50 Lakhs and this is your first house.

Besides, under-construction houses generally quote a lower price than constructed ones. To claim the home loan tax benefits under the two sections, the owner/co-owners of the property must also be the joint borrower/co-borrower to the housing loan. They all must be co-owners of the property and further it helps in the larger tax claim benefits if in the family itself. Interest on home loan deduction in income tax for under construction property is not available for the repairs/renovations/renewals/reconstruction of the property. Sec 24b of income tax act deals with the housing loan interest tax exemption.

The borrower must not be the owner/co-owner of any other pucca house. Maximum deduction under 80C that can be claimed by the borrower in a year is up-to Rs.1.5 Lakhs. Taking a home loan can help you save tax as per the provisions of the Income Tax Act, 1961. Even more so after the announcements made during the latest financial budget. Yes, if the property is registered in both names and if she is also a co-borrower in the home loan. According to the Finance Bill, if a unit is located in a metropolitan city, its carpet area should not exceed 645 sq ft or 60 sq metres, to claim the Section 80EEA benefit.

The municipal taxes borne and actually paid during the financial year are allowed as the deduction from “annual rental value” of the house property. For claiming deduction u/s 80EE, property value must be below than Rs. 50lacs. So, as your property value exceeds the threshold limit, you are not eligible to claim interest deduction u/s 80EE.

HDFC give me an interest certificate as a first borrower. Deduction u/s 24 & 80C is available only after the house property constructed/acquired. Since both possession and payment has been made in 2013, the purchase will be deemed to be in the year 2013. In my case, I own two houses but stay in the rented house. I am using the 80C section for Repayment of Housing Loan and using it upto 1.5 lakhs. Deduction u/s 80C is available only where the loan is taken for acquisition or construction of residential house.

The property value must not exceed Rs 50 lakhs and the loan value should be up to Rs 35 lakhs.3. Deductions can only be claimed if the loan is borrowed from a financial institution. Rebate is not applicable if the loan is borrowed from family members or friends.4. Tax payer can claim the rebate under Section 80EE only after exhausting the waiver provided under Section 24. If a property is jointly owned, each co-borrower can claim Rs 2 lakhs as tax deduction on their respective incomes under Section 80C. In this case also, all the owners have to be co-borrowers.

No comments:

Post a Comment